Dr. Bitan Ghosh spent over a decade watching promising startups get rejected for the wrong reasons, and built the Elevent Index to separate a genuinely good business from one that simply looks investment-ready on paper.

There is a particular kind of failure that haunts early-stage investing, and it rarely makes it into the post-mortem. A startup with a real product, a real market and a founder who clearly knows the business gets turned down, not because the opportunity was weak, but because the pitch deck was sloppy, the cap table was a mess, and nobody on the founding team had thought to organize the data room before walking into the room. Somewhere else, the opposite happens: a startup with a beautifully rehearsed pitch and immaculate paperwork raises a round it probably shouldn’t have, because the underlying business never had the traction its slides implied.

Dr. Bitan Ghosh, an entrepreneur, independent researcher and business strategist who has spent more than twelve years around startups and the people who fund them, built the Elevent Index because he kept watching both versions of that story play out, and became convinced the industry didn’t actually have a shared way to tell them apart.

A problem hiding in plain sight

Ask any two investors what makes a startup fundable, and you’ll get two different checklists. One leans on founder pedigree, another on market size, a third won’t move past unit economics. That variation isn’t necessarily a bad thing. Investing is a craft, and craft implies judgment. But it does mean two firms can look at the exact same company and land in entirely different places, and neither one can fully explain to the other why.

Dr. Ghosh’s answer starts from a distinction that sounds obvious once you hear it, and turns out to be almost entirely absent from how due diligence actually gets done: how good a business is, and how ready that business is to raise money from institutional investors, are two different questions. Most evaluation processes quietly treat them as one. The Elevent Index insists on keeping them apart.

Two scores, then one decision

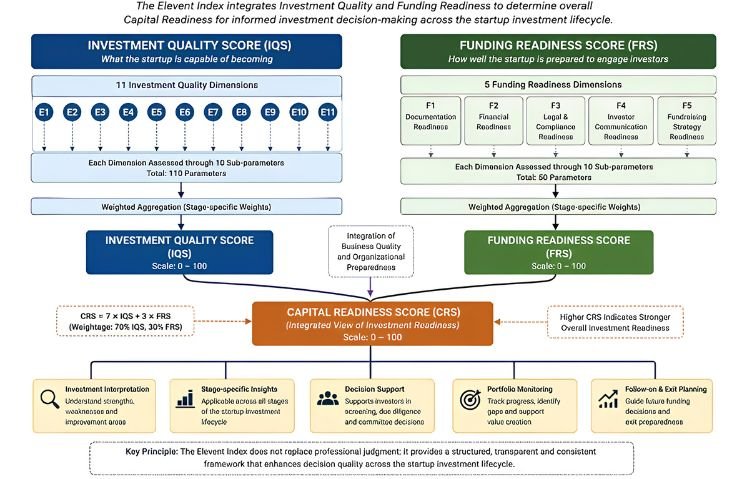

The framework runs on three numbers. The first, the Investment Quality Score, asks what the startup is capable of becoming, evaluated across eleven dimensions that range from founder and leadership strength and market opportunity to governance, customer traction and long-term sustainability. The second, the Funding Readiness Score, asks something narrower and, in Dr. Ghosh’s view, chronically underrated: can this organization actually be evaluated efficiently by an outside investor, based on its documentation, its financial reporting, its legal housekeeping and how clearly it communicates with people writing checks. The two combine into a Capital Readiness Score, weighted so that business quality still counts for more, because no amount of polish invents a market that isn’t there, but a genuinely strong company can absolutely lose a round it deserved to win over a cap table nobody bothered to clean up.

Run that lens across real-world situations and the payoff becomes obvious fast. A technically gifted startup with an unfinished governance structure doesn’t get told no. It gets told exactly what to fix, and in what order, before it walks back into a boardroom. A startup with a gorgeous investor deck sitting on top of thin customer validation doesn’t get mistaken for something more solid than it is. The framework’s real innovation isn’t the scoring. It’s the refusal to let a single verdict, invest or pass, flatten two very different diagnoses into the same outcome.

Built to follow a company, not just judge it once

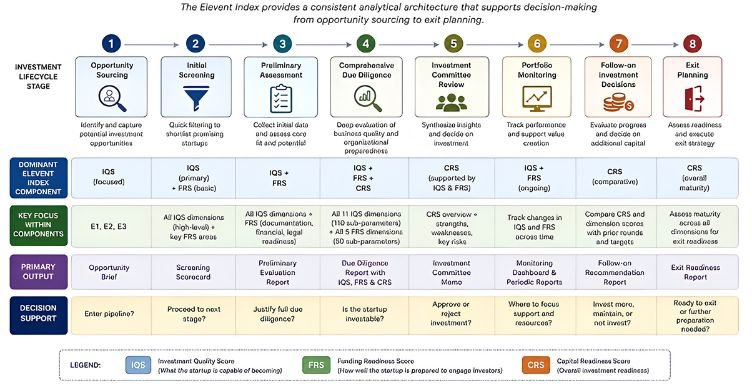

What separates the Elevent Index from the usual internal scorecard is that Dr. Bitan Ghosh didn’t design it to end at the term sheet. Most due diligence tools are built for one moment, the weeks right before money changes hands, and then get abandoned the second the wire clears, replaced by a completely different set of portfolio metrics. That handoff is where a lot of institutional memory quietly disappears.

Dr. Ghosh built the Elevent Index to run continuously instead, tracking the same underlying architecture from the first time a startup crosses an investor’s desk through screening, full due diligence, the investment committee, ongoing portfolio monitoring, follow-on rounds and eventually an exit, with the emphasis shifting as the company grows up. Early on, when a founder and an idea are most of what exists, leadership and market opportunity carry the weight. Later, when a fund is deciding whether to double down, the more useful signal is whether the Capital Readiness Score is actually trending upward round over round, evidence the company is maturing rather than just getting bigger. That continuity means an investor isn’t rebuilding their evaluation logic from scratch every time a portfolio company hits a new stage, and a founder gets to see, in concrete terms, whether the work they put in after the last round actually moved the needle.

Why founders may end up as the framework’s biggest fans

Most due diligence has always been something that happens to founders, not something built for them. Dr. Ghosh flips that. Because the framework identifies specific weaknesses rather than issuing a flat rejection, weak governance, thin documentation, an underbaked fundraising strategy, it gives entrepreneurs an actual roadmap instead of a closed door. That’s a meaningfully different conversation than the standard “not ready yet,” and it reframes fundraising as something a founder can systematically work toward rather than a talent for pitching they either have or don’t.

That same design travels well beyond venture capital. Angel investors and family offices, who rarely have large analytical teams behind them, get a structured way to evaluate deals instead of leaning entirely on gut instinct. Accelerators get a way to prove their cohorts are genuinely improving, not just finishing a program. Banks evaluating venture debt get visibility into organizational risk that a balance sheet alone won’t show them. Government agencies handing out innovation grants to hundreds of applicants get a consistent basis for comparison across sectors no single reviewer could specialize in.

The bigger bet

What Dr. Ghosh is really proposing is less a scoring tool than a shared language, the kind a maturing startup ecosystem eventually needs if investment decisions are going to rest on the strength of the reasoning behind them, rather than on which analyst happened to read the deck that morning, or which founder happened to have a slicker deck than the business underneath it deserved. Whether the Elevent Index becomes that language is still an open question. But the problem it’s aimed at, the gap between a good business and a fundable one, is one almost everyone in venture capital has quietly lived through, which may be exactly why it’s getting attention now.

To learn more about the framework visit www.eleventindex.com